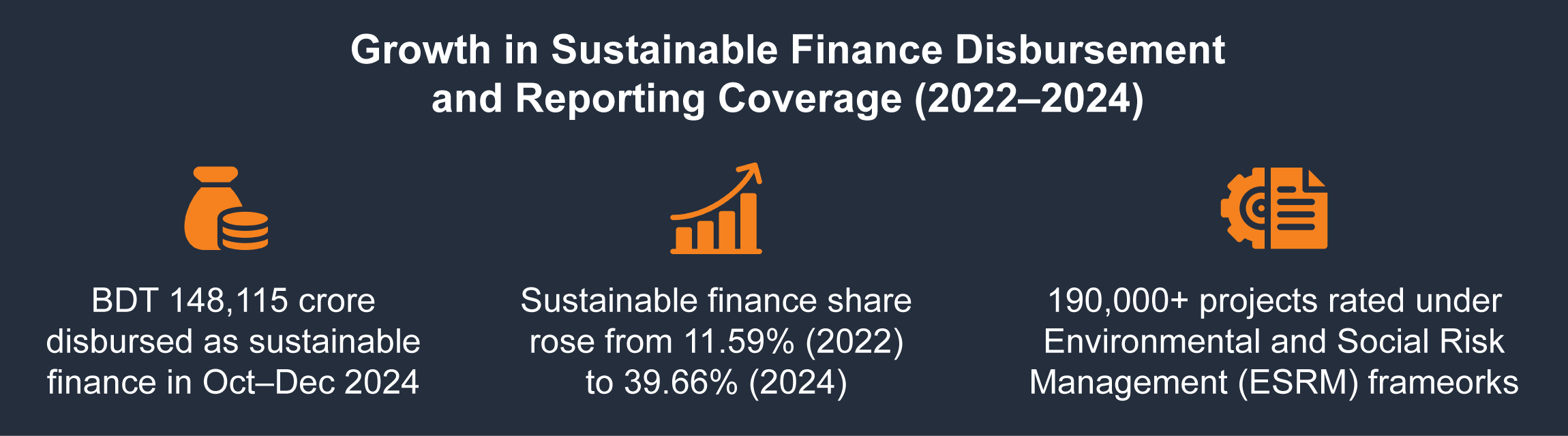

Bangladesh Bank’s Sustainable Finance Reports indicate that, sustainable finance disbursement reached BDT 148,115.22 crore in the October–December 2024 quarter, accounting for approximately 40.66% of total loan disbursement during that period, while annual data show the share rising from 11.59% in 2022 to 17.23% in 2023 and 39.66% in 2024; however, these disbursements fall within the regulatory categories of green and sustainable finance and do not constitute climate finance as defined under internationally recognized taxonomies or disclosure frameworks such as TCFD, indicating that alignment with global climate finance standards remains limited.

Climate change is increasingly recognized as a financial risk. Globally, banks are being asked not only to support green investments, but also to assess how climate-related shocks and transition policies may affect their loan portfolios, capital strength, and long-term resilience.

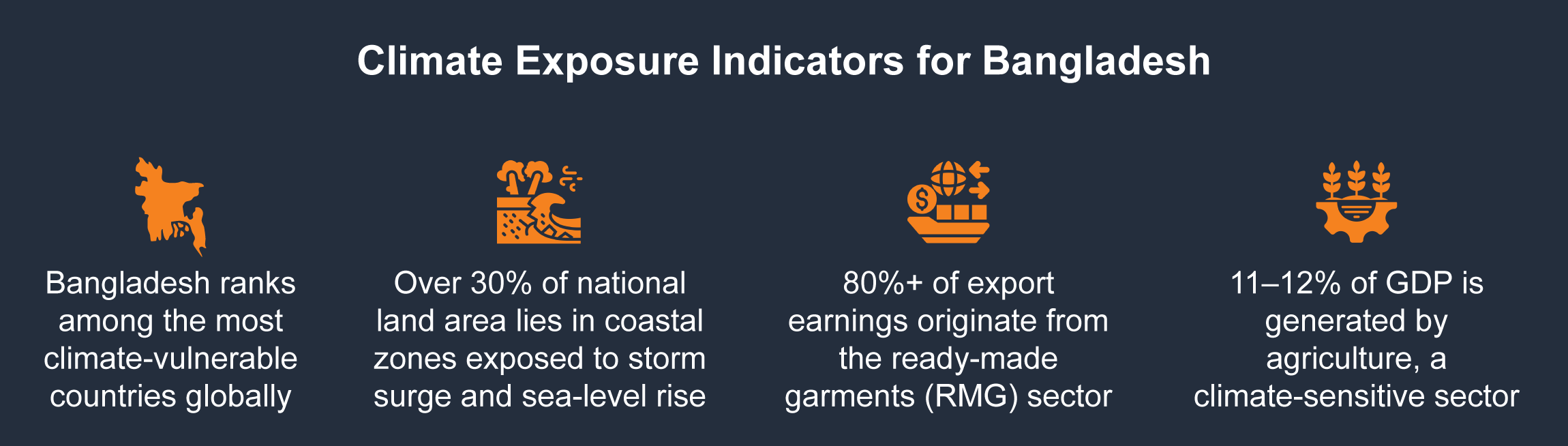

For Bangladesh, this shift carries particular significance. Bangladesh consistently ranks among the most climate-vulnerable countries in global indices. The Notre Dame Global Adaptation Initiative (ND-GAIN) Index places Bangladesh among countries with high exposure to climate risk relative to adaptive capacity. According to assessments by the World Bank and the IPCC, rising flood intensity, cyclones, salinity intrusion, and heat stress are projected to intensify over the coming decades, with direct implications for agriculture, infrastructure, and coastal economic zones.

At the same time, the banking system continues to finance sectors such as agriculture, textiles, infrastructure, real estate, and SMEs, sectors structurally sensitive to both physical climate impacts and global transition pressures. The ready-made garments (RMG) sector alone accounts for more than 80% of Bangladesh’s export earnings, increasing exposure to carbon-related trade measures and global decarbonization policies.

The strategic question is therefore evolving: Is the sector moving beyond green activity reporting toward meaningful climate risk management?

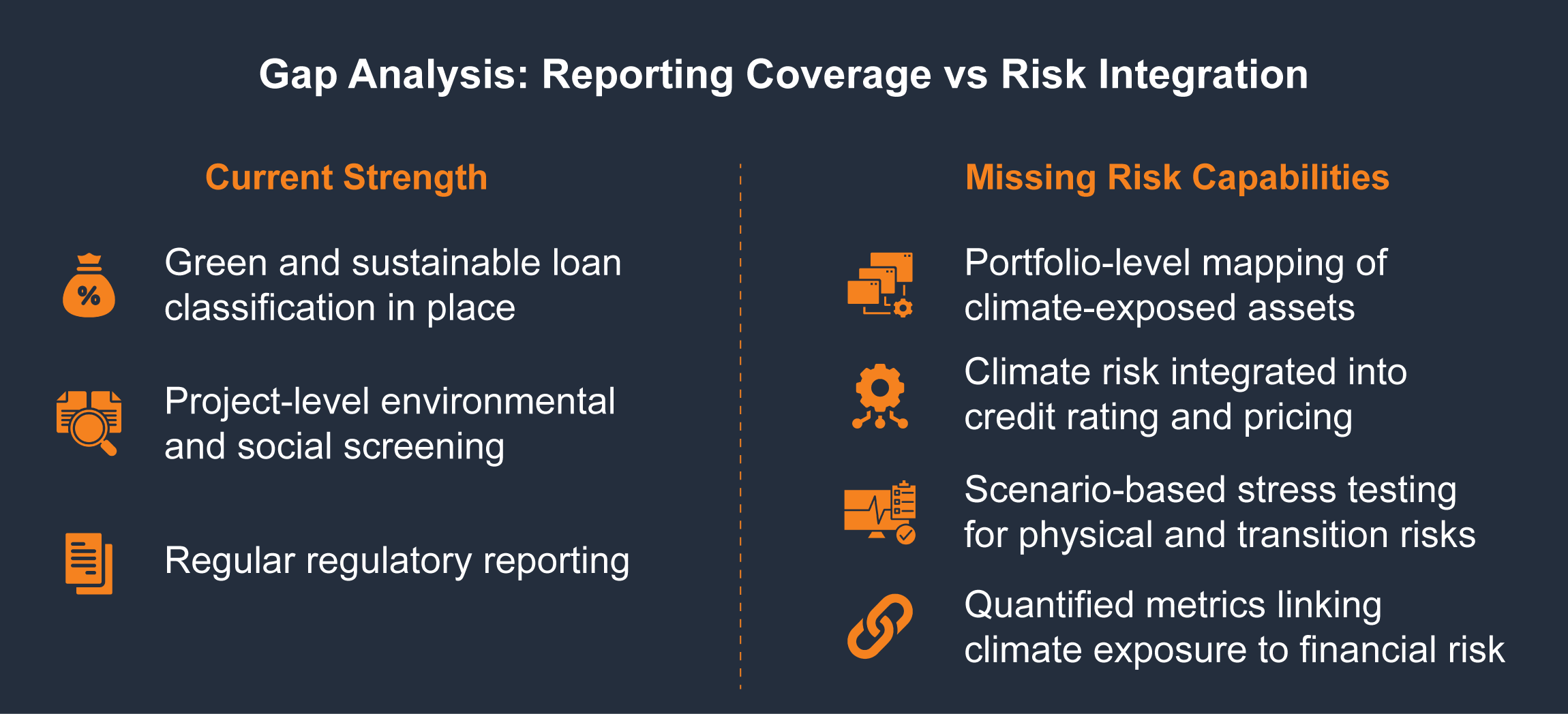

Over the past decade, Bangladesh Bank has established a robust foundation for sustainable finance. Green banking guidelines, Environmental and Social Risk Management frameworks, and structured sustainable finance reporting requirements are now embedded within regulatory practice. These measures have enabled banks to track the volume of green and sustainable lending and to demonstrate progress in allocating capital toward environmentally aligned sectors.

Tracking the volume of green finance indicates what has been funded. Climate risk disclosure under IFRS S2, however, requires a more comprehensive understanding of how vulnerable the broader loan portfolio is to physical and transition risks. This includes geographic concentration in climate hazard zones, noting that over 30 percent of Bangladesh’s land area lies in coastal regions exposed to sea level rise and storm surges. It includes sectoral sensitivity to extreme weather, particularly given that agriculture contributes approximately 11 to 12 percent of GDP and remains highly climate sensitive. It also requires assessing export exposure to carbon-related trade measures, especially in RMG and manufacturing, as well as potential collateral value deterioration under repeated climate shocks.

This shift demands a deeper analytical layer. While the identified challenges are largely relevant and reflect current banking realities, several additional practical gaps merit attention. Data availability and reliability for Scope 3 greenhouse gas emissions, particularly financed emissions, remain limited. Internal capability to conduct forward-looking climate scenario analysis is still developing. Moreover, climate risk considerations are not yet consistently integrated into credit appraisal and risk assessment processes. Addressing these gaps through structured methodologies, capacity building, and cross-departmental coordination would make the IFRS S2 reporting process more rigorous, harmonized, and strategically aligned with risk management objectives.

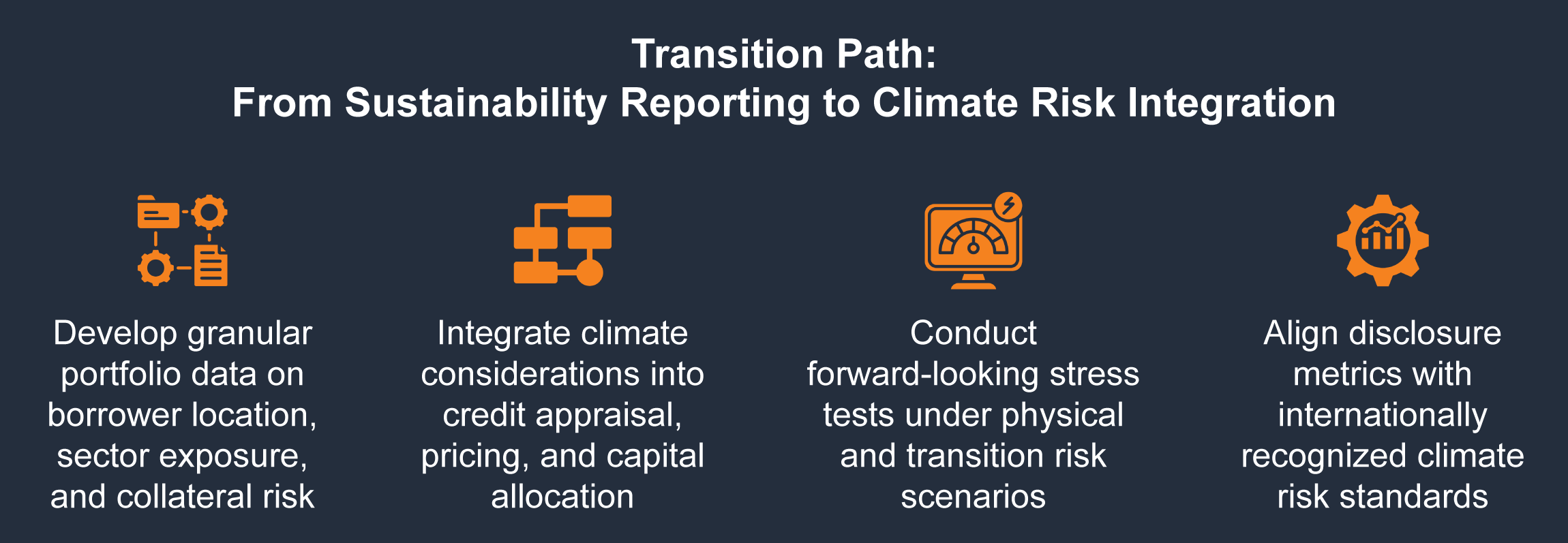

Moving from disclosure-oriented sustainability reporting to genuine climate risk management requires a substantive strengthening of institutional capabilities across the banking system. First, banks must develop granular, portfolio-level data systems that capture borrower location, sectoral exposure, collateral characteristics, and vulnerability to physical and transition risks, enabling meaningful mapping of climate-sensitive assets rather than relying on aggregate classifications. Second, climate considerations need to be systematically embedded into credit appraisal, risk rating, and pricing frameworks, so that exposure to high-carbon or climate-vulnerable sectors directly influences lending decisions, capital allocation, and provisioning practices. Third, institutions must adopt forward-looking stress testing methodologies that model plausible climate scenarios, including extreme weather events, carbon pricing shocks, and regulatory transitions, thereby assessing potential impacts on asset quality, liquidity, and capital adequacy. Finally, banks require clear, consistent, and internationally aligned metrics that link sustainability performance to measurable financial risk, ensuring that climate exposure is quantified, monitored, and reported in ways that inform strategic decision-making rather than remaining a compliance exercise.

Bangladesh Bank reporting shows that environmental and social risk assessments are conducted at scale, with more than 190,000 projects rated in recent reporting periods. This demonstrates procedural coverage. The remaining question is whether these ratings systematically influence probability of default, capital allocation, and portfolio strategy.

While governance structures are in place, integration into core risk systems remains at an early stage across much of the sector.

In practical terms, Bangladesh’s banking system has made significant progress in sustainable finance reporting. The next phase is embedding climate risk within financial decision-making.

Climate risk affects asset quality, capital adequacy, and earnings stability. The World Bank estimates that climate change could reduce Bangladesh’s GDP by up to 9% by 2050 under high-impact scenarios, with concentrated effects in agriculture, infrastructure, and coastal industries. Such macro-level stress inevitably transmits into financial sector balance sheets.

Climate risk is therefore not a communications exercise. It is a risk architecture issue.

Institutions that internalize climate risk within credit models and portfolio strategy will be better positioned to manage volatility, attract long-term capital, and maintain financial resilience. Those that treat it primarily as a reporting requirement may face growing exposure over time.

For Bangladesh, where climate exposure is systemic rather than peripheral, strengthening climate risk integration within the banking sector is not optional. It is central to financial stability and long-term competitiveness.

The foundation has been laid. The depth and speed of integration will determine the sector’s readiness for the years ahead.

Author: Yeasir Arafat Tuhin, an Associate in the Inclusive Financia Solutions (IFS) Portfolio at Innovision Consulting.

.png)